What This Use Case Is — and What It Is Not

Autonomous procurement AI supplier risk scoring is a specific, bounded application: continuous, multi-signal, automated scoring of supplier health across a portfolio, with autonomous escalation to human review when scores breach defined thresholds. The system operates without waiting for a quarterly review cycle or a procurement analyst to initiate a query.

This use case is distinct from three adjacent activities that are frequently conflated with it. First, manual periodic scoring — spreadsheet-based assessments, one-time vendor audits, or annual supplier surveys — is not autonomous and does not provide continuous coverage. Second, broader supply chain risk management platforms that monitor logistics disruptions, port closures, or demand volatility operate at the network level rather than at the individual supplier scoring level. Third, the combination of supplier risk scoring with spend analytics — where risk signals inform category strategy and sourcing decisions simultaneously — is a related but separate use case covered in the AI Supplier Risk Scoring and Spend Analysis entry on ChainSignal.

Within the SCOR framework, this use case maps to the Source process — specifically the supplier evaluation and qualification sub-processes that run continuously rather than at contract renewal. The output of the scoring system feeds into procurement governance workflows: human reviewers receive escalated supplier flags with supporting evidence, not raw data.

How the Use Case Works

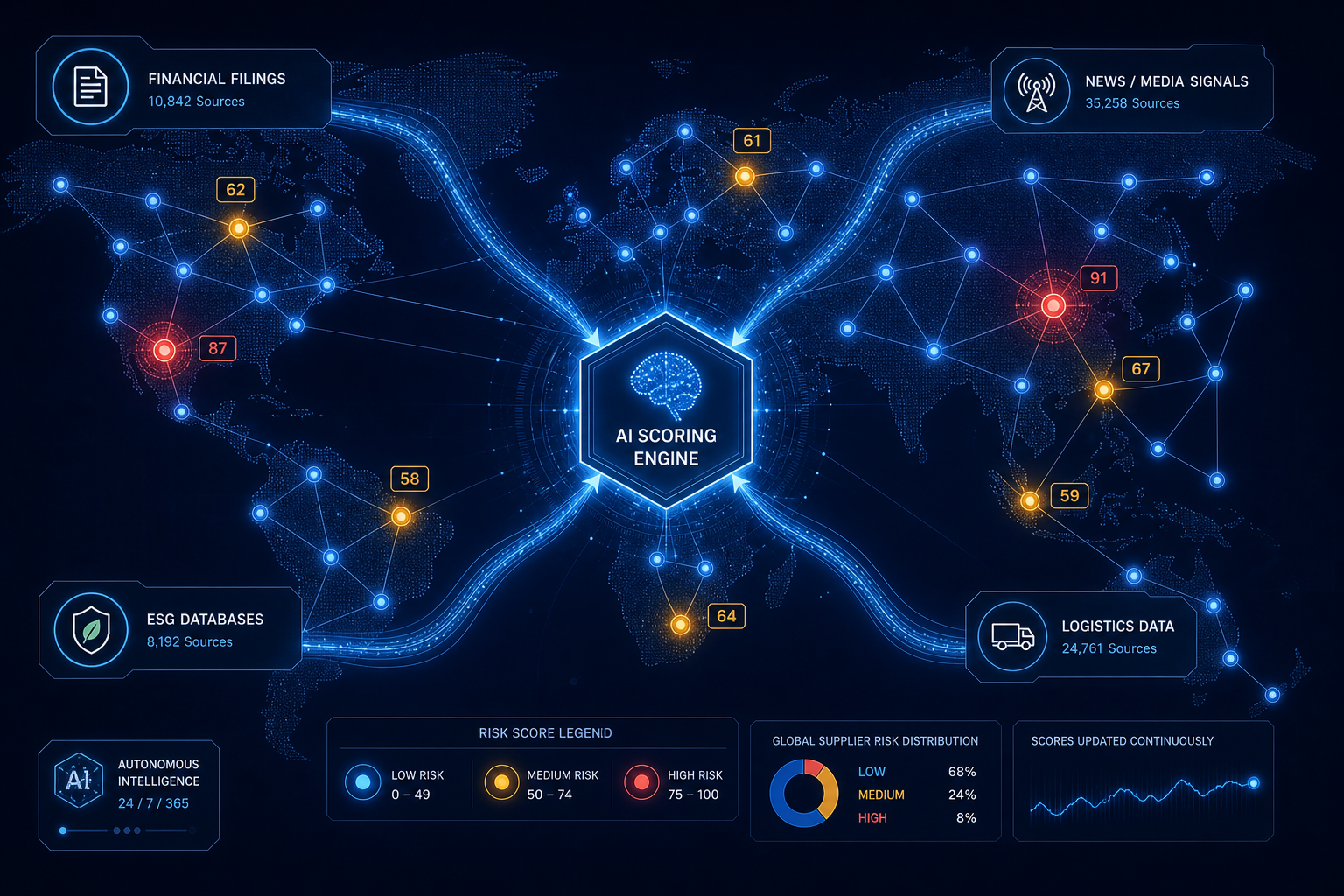

The system scores each supplier across five risk dimensions simultaneously, drawing on signals that no periodic human review process can monitor at the required frequency.

- Financial distress: Declining operating cash flow, shrinking EBIT margins, rising Days Payable Outstanding, and increasing Days Sales Outstanding are tracked continuously. These signals can provide 3–6 months of lead time before a supplier's operational failure becomes visible through missed deliveries.

- Geopolitical exposure: Sanctions screening, trade policy shifts, and regional instability indicators are monitored across the supplier's operating geographies and their known sub-tier dependencies.

- ESG compliance: Adverse media scanning, third-party audit data, and certification renewal tracking identify patterns of labor violations or environmental incidents before regulatory action occurs.

- Operational resilience: Delivery performance trends, capacity constraint signals, and cybersecurity incident exposure are scored against baseline expectations for each supplier segment.

- Sub-tier concentration risk: AI analyzes trade records and shipping data to map hidden dependencies — identifying cases where multiple Tier-1 suppliers share the same sub-tier manufacturer, creating a single point of failure that no Tier-1 audit would surface.

What distinguishes autonomous AI scoring from conventional risk monitoring is the persistence of state. Unlike a query-based tool that responds to a specific prompt, agentic AI maintains continuous awareness of each supplier's risk trajectory — retaining the fact that a supplier failed a compliance check three weeks ago, that its financial indicators have been deteriorating for two quarters, or that a geopolitical event has elevated exposure in a specific sourcing region. This persistent state enables the system to detect deteriorating trajectories rather than only point-in-time anomalies.

When a supplier's composite score crosses a defined threshold, the system autonomously escalates the case to human review — surfacing the specific signals that drove the flag, the confidence level, and the recommended response options. Human gateways are built in for complex and high-value decisions; the system does not autonomously terminate supplier relationships or execute sourcing changes. For readers who need model-level detail on scoring architectures and signal weighting, the Practitioner's Guide to AI Supplier Risk Scoring covers those dimensions.

Where It Delivers Measurable Value

The business problem this use case addresses is large. McKinsey & Company calculates that supply chain disruptions cost 45% of one year's profits over a ten-year period — a figure that frames why continuous supplier monitoring carries executive-level attention. One-third of organizations have experienced annual supply chain disruption losses exceeding €1 million, yet most are still operating reactive systems built to respond to disruptions rather than anticipate them.

Outcome evidence for this use case comes primarily from vendor-reported figures, which should be interpreted with that attribution in mind. Everstream Analytics reports that organizations implementing AI-driven procurement risk management have achieved a 30% reduction in revenue losses from supply disruptions and a 50–70% reduction in the time required to identify and assess disruption impacts. These figures are vendor-reported and not independently benchmarked, but they represent the most specific documented outcome data available for this use case at this maturity stage.

| Outcome Metric | Reported Figure | Source | Attribution Type |

|---|---|---|---|

| Reduction in disruption-related revenue losses | 30% | Everstream Analytics, 2025 | Vendor-reported |

| Reduction in time to identify and assess disruption impacts | 50–70% | Everstream Analytics, 2025 | Vendor-reported |

| Lead time before financial distress becomes operational failure | 3–6 months | JAGGAER continuous intelligence scenarios | Vendor-reported |

| Supply chain disruption cost over a decade | 45% of one year's profits | McKinsey & Company (cited in Everstream, 2025) | Analyst research |

| Average enterprise investment per supplier risk AI use case | $2.0 million | ISG 2025 State of Enterprise AI Adoption | Research study |

| Supplier risk AI use cases in production | 58% | ISG 2025 State of Enterprise AI Adoption | Research study |

| Procurement workload increase vs. budget increase gap | 10% workload / 1% budget | Hackett Group | Research study |

The financial distress scenario illustrates the mechanism behind the lead-time advantage. AI monitoring of liquidity indicators — operating cash flow trends, EBIT margin compression, DPO and DSO movements — can signal supplier financial deterioration months before missed deliveries occur, giving procurement teams time to qualify alternative sources rather than scrambling after a disruption. The ESG monitoring dimension delivers a different type of value: continuous adverse media scanning and audit deviation detection reduce the risk of regulatory exposure under frameworks like CSDDD and Germany's LkSG, where buyers bear due diligence obligations for their supply chains.

Applicable Industries and Documented Deployment Contexts

Autonomous supplier risk scoring has documented deployments or strong evidenced fit across five industry verticals. The primary risk driver differs by industry, which shapes how organizations configure scoring weights and escalation thresholds.

- Automotive: Sub-tier concentration risk is the primary driver. Automotive supply chains have deep multi-tier structures where a single specialty component manufacturer may supply multiple Tier-1 suppliers simultaneously, creating hidden single points of failure that are invisible without AI-driven network mapping. The 2021 semiconductor shortage demonstrated the cost of this blind spot at industry scale.

- Pharma and life sciences: Regulatory compliance monitoring and agricultural yield forecasting are the primary drivers. Everstream Analytics has developed crop-sourcing intelligence capabilities specifically with leading pharmaceutical clients — predicting agricultural yield and quality months before harvest to anticipate active ingredient supply constraints. This represents one of the most specifically documented cross-industry deployments of AI-driven supplier intelligence available.

- Food and beverage: Crop-sourcing intelligence (developed alongside F&B clients by Everstream) addresses the same yield forecasting problem as pharma but applied to commodity ingredients. Geopolitical exposure monitoring is also material, given the geographic concentration of many agricultural inputs.

- Retail and CPG: Operational resilience and ESG compliance are the primary drivers, with growing regulatory pressure under supply chain due diligence legislation requiring documented monitoring of supplier labor and environmental practices.

- Electronics manufacturing: Geopolitical exposure and sub-tier concentration risk dominate, given the geographic concentration of semiconductor and rare earth supply chains and the trade policy volatility affecting key sourcing regions.

Adoption Maturity

This use case is classified as Growing, approaching Established — the most mature of the procurement-adjacent AI use cases by production deployment rate.

The ISG 2025 State of Enterprise AI Adoption study, drawn from analysis of 1,200 AI implementations, found that supplier risk assessment and monitoring has the highest production deployment rate among all procurement-adjacent AI use cases: 58% of use cases in production, with average investments of $2.0 million per use case. For comparison, supplier management — a related but distinct function — accounts for 4% of AI use cases but only 8% have reached production status despite average investments of $2.6 million per use case.

| Use Case | Share of Enterprise AI Use Cases | Production Rate | Avg. Investment |

|---|---|---|---|

| Supplier risk assessment and monitoring | 3% | 58% (highest) | $2.0M |

| Supplier management | 4% | 8% | $2.6M |

| Procurement (all functions) | 6% of enterprise AI total | Varies by sub-function | Varies |

The 58% production rate is a meaningful signal, but the 3% share of enterprise AI use cases by volume indicates that procurement overall — and supplier risk scoring within it — remains underpenetrated relative to other enterprise functions. Procurement represents just 6% of AI use cases across all enterprise functions, which means the early-mover advantage window remains open for organizations that move now.

The constraint on faster maturity progression is data readiness. Gartner research finds that 74% of procurement leaders report their data is not AI-ready — a figure that explains the gap between high production rates among early adopters and limited overall penetration. The Hackett Group's finding that procurement workloads have increased 10% while budgets have increased only 1% adds a demand-side driver: the efficiency gap is creating organizational pressure to automate that will accelerate adoption regardless of data readiness challenges.

Representative Vendor Landscape

The vendor landscape for autonomous supplier risk scoring spans four platform categories. The categories differ in scope, integration model, and the depth of their native risk intelligence capabilities. For a comparison of the underlying AI methodologies — rule-based, machine learning, graph-based, NLP, and hybrid approaches — across these categories, see the Procurement AI Supplier Risk Scoring: Methods Compared article.

| Platform Category | Representative Vendors | Primary Differentiator | Typical Buyer Fit |

|---|---|---|---|

| Pure-play supply chain risk intelligence | Everstream Analytics, Prewave, Gainfront | Depth of native risk signal coverage; analyst-augmented intelligence (Everstream); real-time monitoring breadth | Enterprises with complex global supply chains needing standalone risk intelligence |

| Source-to-pay suites with embedded risk modules | JAGGAER, Ivalua, Coupa | Risk scoring integrated within existing procurement workflow; no separate tool deployment required | Organizations already on a source-to-pay platform seeking to activate embedded risk capabilities |

| Trade data and network mapping specialists | Altana, Exiger | Sub-tier visibility through trade data; sanctions and compliance screening depth | Organizations with regulatory compliance exposure or complex multi-tier mapping requirements |

| Orchestration and intake layers with risk scoring | Zip | Risk signals embedded in intake and requisition workflows; procurement process orchestration | Organizations prioritizing intake-to-procure automation with risk as one embedded signal |

Everstream Analytics combines AI, NLP, and predictive modeling with domain specialists — supply chain analysts, meteorologists, and logistics experts — to deliver contextual risk intelligence beyond automated alerts. Its integrations with SAP and Oracle are documented, and its crop-sourcing intelligence capability for F&B and pharma clients represents one of the most specifically evidenced cross-industry deployments in this vendor category. The 2026 Gartner Magic Quadrant recognition (second consecutive year as a Leader) is one reference point among several for evaluating pure-play platforms; it should not be treated as a definitive ranking.

Key Implementation Risks

Five failure modes are most relevant for stakeholder validation. Each is named and briefly characterized here; detailed guidance on each is available in the linked ChainSignal articles.

- Training data bias against non-Western and SME suppliers. A 2022 study published in Nature Machine Intelligence found that NLP models used in corporate ESG screening exhibited language and geographic bias, particularly against suppliers in non-OECD countries — bias that is rarely visible to end users but may influence supplier exclusion decisions. Organizations with globally distributed supply bases should require vendors to disclose training data composition and geographic coverage.

- False positives from poor entity resolution. A documented case: a European public buyer excluded a Tunisian SME after it was flagged for elevated reputational risk. Manual review revealed the flag originated from an outdated media report referencing an unrelated company with a similar name — a failure of entity resolution in the AI model's training data. False positive rates that are acceptable in a portfolio of 500 suppliers become operationally disruptive in a portfolio of 5,000.

- Explainability gaps under CSDDD and LkSG regulatory requirements. Under the EU Corporate Sustainability Due Diligence Directive and Germany's Supply Chain Act, buyers bear documented due diligence obligations. AI tools that cannot explain which signals drove a risk flag — and at what confidence level — create regulatory exposure, not just operational uncertainty. Leading organizations now require AI scoring tools to offer explainable outputs aligned with ISO/IEC 42001.

- ERP integration complexity across legacy systems. Supplier master data is typically fragmented across ERP, procurement, and finance systems — often with inconsistent supplier identifiers, duplicate records, and incomplete coverage of the active supplier base. Integration depth directly determines the quality of financial distress and operational resilience signals available to the scoring model.

- Data readiness. Gartner finds that 74% of procurement leaders report their data is not AI-ready. This is not a technology limitation — it is an organizational and process prerequisite that must be addressed before deployment, not during it. For detailed guidance on data prerequisites, see the Data Requirements and Deployment Conditions for AI Supplier Risk Scoring.

Readiness Indicators and Related Use Cases

Organizations that are ready to evaluate this use case typically share several characteristics. Those that lack these prerequisites will see implementation timelines extend significantly and outcomes fall short of benchmarks.

- A consolidated, deduplicated supplier master with consistent identifiers across ERP and procurement systems — the minimum data foundation for reliable entity resolution and financial signal extraction.

- Defined risk thresholds and escalation workflows that procurement leadership has agreed to in advance — without these, autonomous escalations will create organizational friction rather than faster response.

- Clarity on regulatory due diligence obligations (CSDDD, LkSG, or sector-specific requirements) that will govern explainability and audit trail requirements for the scoring system.

- Executive sponsorship that treats supplier risk as a strategic input to sourcing decisions, not a compliance checkbox — organizations that deploy risk scoring without connecting it to sourcing authority see limited adoption of escalated flags.

- A defined scope for the initial deployment: a specific supplier segment (critical single-source suppliers, high-spend categories, or geographically concentrated sourcing) rather than full-portfolio coverage from day one.

Organizations that do not yet have a consolidated supplier master or defined escalation governance should treat data readiness and process design as Phase 1 before evaluating vendors. The AI Supplier Risk Scoring Implementation Guide for Mid-Market Procurement Teams provides a size-appropriate deployment roadmap for organizations with $200M–$2B in revenue.

For organizations evaluating both supplier risk scoring and spend analytics simultaneously — a common pairing when procurement AI initiatives are initiated at the category or CPO level — the AI Supplier Risk Scoring and Spend Analysis use case entry covers the combined use case and the sequencing decisions that determine which capability to activate first.

Comments

Join the discussion with an anonymous comment.